Determination of the objectives of the pricing policy Pricing policy does not imply

The purpose of a commercial enterprise is to make a profit. The company earns its income from the sale of goods and...

Corporations - Fund for Assistance to the Reform of Housing and Communal Services

1. General provisions

This Regulation on improving investment and operational efficiency and reducing the costs of the state corporation - the Fund for Assistance to the Reform of Housing and Communal Services (hereinafter referred to as the Fund, Regulation) was developed in pursuance of subparagraph "b" of paragraph 2 of the list of instructions of the President Russian Federation dated December 27, 2014

No. Pr-3013 and instructions of the Government of the Russian Federation dated March 23, 2015 No. ISH-P13-1818 and dated June 24, 2015 No. ISH-P13-4148, taking into account the Guidelines for the preparation of the Regulations for improving investment and operational efficiency and reducing costs.

The regulation is aimed at organizing a continuous process of improving investment and operational efficiency and reducing costs.

The Regulation establishes the procedure for the development, formation, monitoring, control and approval of the Program for improving the investment and operational efficiency and reducing the costs of the Fund (hereinafter referred to as the Program).

2. Terms and Definitions

For the purposes of this Regulation, the following basic concepts are used:

The investment activity of the Fund is the investment of temporarily free funds of the Fund in order to preserve them and minimize losses from depreciation due to inflation.

Investment efficiency - maximization of the result (financial and non-financial) in the framework of investment activities in relation to the costs incurred.

The operational activity of the Fund is the provision of financial support to the constituent entities of the Russian Federation, the implementation of outreach and other activities aimed at educating citizens in the field of housing and communal services, assistance in training personnel in the field of housing and communal services, providing activities, as well as other activities aimed at to fulfill the goals and objectives of the Fund established by the legislation of the Russian Federation and the Long-term program of activity and development of the Fund, approved by the Supervisory Board of the Fund on April 29, 2014, protocol No. 42 (hereinafter referred to as the Long-term Program).

Operational efficiency is the ratio of the result achieved to the established goals and objectives of the activity while reducing overall costs.

Cost centers are structural subdivisions assigned to certain types of operational activities or separate areas (activities), in accordance with which costs are incurred, and in relation to which goals for increasing efficiency and reducing costs can be specified.

Key performance indicator (KPI) is an indicator of the achievement of planned results used to determine the effectiveness of the Program as a whole and individual activities within the framework of the Program, which can be quantified and is significant from the point of view of the goals and objectives of the Fund.

3. Regulatory and other documentation

The following documents were used in the development of the Regulations:

− Federal Law No. 185-FZ of July 21, 2007 “On the Fund for Assistance to the Reform of the Housing and Utilities Sector” (hereinafter referred to as the Federal Law);

− Federal Law of January 12, 1996 No. 7-FZ “On non-commercial organizations”;

− Federal Law of July 18, 2011 No. 223-FZ “On Procurement of Goods, Works, Services by Certain Types of legal entities»;

− Decree of the President of the Russian Federation of May 7, 2012 No. 600 “On measures to provide citizens of the Russian Federation with affordable and comfortable housing and improve the quality of housing and communal services”;

− Government program of the Russian Federation “Providing affordable and comfortable housing and utilities for citizens of the Russian Federation” (approved by Decree of the Government of the Russian Federation of April 15, 2014 No. 323);

− Decree of the Government of the Russian Federation dated December 21, 2011 No. 1080 “On Investing Temporarily Free Funds of a State Corporation, State Company”;

− Decree of the Government of the Russian Federation dated February 21, 2013 No. 147 “On the procedure for granting subsidies in the form of property contributions of the Russian Federation to the state corporation - the Fund for Assistance to the Reform of the Housing and Communal Services in 2013-2017 and on the specifics of providing financial support to the constituent entities of the Russian Federation” ( hereinafter - Decree of the Government of the Russian Federation No. 147);

4.1.5. Financing of expenses for ensuring the activities of the Fund is carried out in accordance with federal law No. 185-FZ. The amount of funds necessary to ensure the activities of the Fund is annually established by the Supervisory Board of the Fund.

5. Conditions for the development and implementation of the Program

5.1. The goal of the Program is to organize a continuous process of improving investment and operational efficiency and reducing costs.

5.2. The development of the Program, as well as the introduction of changes to it, are carried out on the basis of proposals received from the structural divisions of the Fund in the relevant areas of their activities and / or events.

5.3. The program is formed in accordance with the goals and objectives of the Fund, established by Federal Law No. 185-FZ and the Long-Term Program, in the following main areas:

− investment activity;

− consideration of applications submitted by the constituent entities of the Russian Federation for the provision of financial support at the expense of the Fund for the resettlement of citizens from dilapidated housing stock, the overhaul of apartment buildings, the modernization of utility infrastructure systems, the adoption of decisions on the compliance of applications and documents attached to applications with the requirements established by Federal Law No. 185-FZ, providing financial support at the expense of the Fund on the basis of applications;

− monitoring the implementation of regional programs and the fulfillment of the conditions for the provision of financial support at the expense of the Fund, stipulated by Federal Law No. 185-FZ;

− methodological support for the preparation by the constituent entities of the Russian Federation of applications and documents attached to applications

− outreach activities;

− assistance in training personnel in the field of housing and communal services;

− personnel management and anti-corruption;

− procurement and ensuring the functioning of the Fund;

− other areas of activity, the effectiveness and cost reduction in which can be recognized as significant from the point of view of the goals and objectives of the Fund.

Measures to improve the efficiency of investment activities are highlighted separately in the Program.

5.4. The program must include the following elements:

− assessment of the current state of investment and operational efficiency;

− the classification of costs adopted for the purposes of the Program implementation by areas (items) of costs, cost centers (structural divisions or activities), as well as by other principles, the application of which will be deemed appropriate in terms of cost control and management;

− priorities and risks associated with cost management for the planning period;

− KPIs for individual activities and the Program as a whole. KPIs are set based on the need to improve efficiency and reduce the Fund's costs. KPIs of activities within the framework of the Program may be included in the system of KPIs of structural units. The KPI of the Program is set based on the need to reduce costs in an amount not less than that provided for by the Long-Term Program.

When evaluating KPIs based on comparing indicators of the current and previous periods, the principle of comparability of data should be observed, in which the components of the indicators that took place in the current period, but were absent in the past, should not be taken into account. The composition, specific content and KPI values are determined on an annual basis.

5.5. Each event of the Program should include a description of the event, the frequency (terms) of its implementation, the required amount of financial resources for the implementation of the event (if any), the planned economic effect (reducing costs, increasing labor productivity, etc.), methods for assessing the results achieved , responsible structural unit and planned KPI.

5.6. If it is planned to allocate financial resources for the activities of the Program that are not provided for by the current documents of the Fund ( financial plan(budget) and estimates of administrative and economic costs), then simultaneously with the planning of such activities of the Program, it is necessary to carry out the envisaged measures to amend the relevant documents.

5.7. In order to form and update the Program, as well as monitor its implementation, the Fund creates a working group on efficiency, which includes employees directly reporting to the General Director and heads of structural divisions. The head of the working group is appointed from among the deputies of the general director.

The functions of the working group are:

− consideration of proposals to improve efficiency and reduce costs and formulate the Program;

− annual monitoring of the implementation of the planned activities of the Program.

The Board of the Fund approves the Program formed by the working group on efficiency for the corresponding period.

5.8. Responsibility for the development and implementation of individual activities of the Program is borne by employees of direct subordination to the General Director and heads of structural divisions of the Fund, which is assigned functions corresponding to the listed areas.

6. Description of the process of forming the Program

6.1. The program is formed and approved annually.

6.2. In order to initiate the formation/updating of the Program, the General Director of the Fund issues an order on the development/updating of the Program for the corresponding calendar year, which should determine:

− composition and leader of the working group on efficiency;

− terms of preparation by the structural subdivisions of the Fund of a list of activities to be included in the Program;

− a structural subdivision responsible for collecting and summarizing proposals within the framework of the formation of the Program;

− a structural subdivision responsible for monitoring the implementation of the Program activities and the achievement of the KPIs provided for by the Program.

6.3. Structural divisions of the Fund, within the established time limits, send to the responsible structural division a list of measures to improve efficiency and reduce costs for the corresponding calendar year, which includes:

− assessment of the current state of the efficiency of the functions performed;

− identifying priority areas for improving operational activities;

− factors influencing operational efficiency;

− the amount of financial resources required for the implementation of activities (if necessary);

− the planned economic effect from the implementation of activities;

− the possibility of forming KPIs for the planned activities.

6.4. The responsible structural subdivision of the Fund, on the basis of the information provided, ensures:

− preparation of summary information on planned activities for inclusion in the Program;

− formation of the draft Program for its consideration by the working group on efficiency;

− conducting a comparative analysis of the achievement of goals and the implementation of planned activities for the implementation of the Program, followed by consideration of the results of the analysis by the working group on efficiency;

− generation of reports on improving efficiency and reducing costs for consideration by the Board and the Supervisory Board of the Fund.

7. Responsibility

Responsibility for the implementation of the Program and its results, expressed in achieving the KPI of the Program as a whole and the KPI of individual activities, are established in accordance with the Regulations on the remuneration of employees of the Fund.

8. Monitoring and control

8.1. In order to assess the implementation of the Program, a system of monitoring and control over the implementation of the activities provided for by the Program is organized.

8.2. The authority to monitor the implementation of the Program and the achievement of KPIs is assigned to the structural subdivision of the Fund, determined by the General Director.

8.3. Structural divisions send information on the progress of the implementation of the Program activities and achieved KPIs on a quarterly basis to the responsible structural division determined in accordance with clause 8.2 of these Regulations, which processes, summarizes and sends the information received to the head of the working group on efficiency and the General Director.

8.4. The evaluation of the progress of the Program implementation is carried out on the basis of the relevant KPIs.

8.5. Control over the implementation of the Program is carried out by the Board of the Fund, general manager and a working group on efficiency.

Increasing operational efficiency is the most important and fundamental task for Russian companies. Its implementation will allow them to significantly raise the level of productivity and competitiveness. Issues of operational efficiency should be constantly in the center of attention of every leader. Improving efficiency is a continuous process that requires deep analysis and rethinking at every stage of a company's development. To succeed in this, Russian companies must fundamentally improve their skills in organizing production. Improving efficiency should become a natural aspiration of every employee, an integral part of the corporate culture of the organization. This approach will allow the company to maintain leadership and reach new frontiers.

We have included in this issue articles summarizing international best practices in areas in which Russian companies are showing an active interest. I would like to draw special attention to two publications.

Model Factories: A Path to the Future describes McKinsey's innovative methodology for developing functional and managerial skills in executives and front-line workers. The essence of the approach is as follows: in workshops specially designed and built for the purposes of training, production lines are installed that can be modified and adjusted, gradually increasing the efficiency of the simulated production in the learning process. In this way, students, together with the instructors of the training center, can implement improvements in practice, gradually establishing an ideal production process and thereby gaining experience in applying various methods of lean manufacturing.

Together with partners - large universities and international companies - McKinsey has created several such training centers around the world: in Germany, France, the USA, China, Singapore, Italy, the Netherlands. A similar project is now being implemented in Russia - jointly with OAO United Machine-Building Plants and the Ural Federal University with the support of the Ministry of Education of the Russian Federation. At the Model Factory in Yekaterinburg, it will be possible to simulate the processes of machining and assembly, production planning procedures for industrial enterprise or even the work of a bank branch and a call center. Factory training will be available to managers and employees from a wide range of companies. The commissioning of the factory is scheduled for early 2015.

The second article that I would like to draw the attention of readers to is an interview with the Director of the Implementation Department production system JSC "Sberbank" Valentin Morozov. Sberbank's transformation program is one of the clearest examples of a successful transformation program being implemented in a large Russian company. Valentin talks about how he managed to mobilize a huge organization to increase efficiency, inspire ordinary employees of departments, and ensure sustainable results. The example of Sberbank once again confirms the universal applicability of approaches to improving operational efficiency, regardless of industry and geography. The main thing is to correctly take into account the specifics of your company (technology, market, business processes), rally the management team around a single goal and start transformations on a systematic basis.

McKinsey's approach to sustainably improve operational efficiency involves transforming three areas simultaneously: the operating system, the management system, and the culture of behavior. The lack of expected results in any of these areas will become an insurmountable obstacle to the successful implementation of the entire program as a whole.

An operating system is the order in which assets, resources, and people are managed to create customer value with minimal waste. For example, the operating system of a manufacturing enterprise includes such components and parameters as standard operating procedures, health and safety regulations, equipment layout, level of its utilization, minimum level of stock balances, normative number of personnel.

The organizational structure, mechanisms for advanced training, setting goals and motivation, as well as other elements of the management system must comply operating system: They should be set to make efficiency gains an ongoing process, not a one-time heroic effort.

Finally, employees' understanding of their work, their attitude towards it, their personal motivation and goals must also comply with the principles of improving efficiency, otherwise the changes will only have a temporary effect. Emotional impact is an essential element of any change program: it is necessary for employees at all levels of the company to understand the causes of change, understand the general direction of movement and are ready to commit themselves to achieving a common goal.

Improving operational efficiency is one of the most important tasks facing the leaders of both private and public companies. Conferences and seminars on the introduction of the principles of lean manufacturing and increasing labor productivity are now constantly held, intended for representatives of federal and regional authorities, heads of industry organizations and major companies. We hope that the articles published in this issue will help you take a few steps closer to achieving your goals and inspire you to further transform.

Anatoly Ermolov- partner of McKinsey, Moscow

Vitaly Klintsov- Managing Partner for Russia McKinsey, Moscow

Operational efficiency

Operational efficiency is an important task for the dynamic development of the company and the achievement of high-quality and efficient service that meets the requirements of the organization's customers in an increasingly competitive environment.

The production efficiency of the enterprise includes several strategies and techniques, the application of which is aimed at providing customers with quality goods and services in a timely manner at minimal cost to the enterprise. Its general aspects include the use of resources, production, distribution of goods, inventory management, and the most important factors determine the direction of the business, for example, production, distribution, retail. To successfully compete with big companies which benefit from economies of scale and greater bargaining power, small businesses need to constantly work to improve operational performance.

Optimal use of resources and elimination of waste in the process of production of goods and in other activities of the company are the main indicators of increasing the effectiveness of the enterprise. From the point of view of the work of the personnel, this means the achievement of the highest productivity of the work of employees in production or in the field of sales. On the other hand, obtaining maximum profit from financial investments in production and efficient use of raw materials are also among the key indicators optimization of company operations. Achieving optimal indicators of production costs and overhead costs is the most important aspect of the formation of a high rate of return.

We develop processes and help determine the optimal resources required for the production and delivery of goods and services in order to achieve a quality and efficient service that meets the requirements of the organization's customers.

Improving the performance of an enterprise specializing in the manufacture of products is impossible without the main component - an effective production process. It involves optimizing the operation of equipment, production processes and personnel in order to achieve maximum production of quality products with a certain amount of capital in a given period of time.

Many manufacturers invest in training their staff in new ways of working according to the concept of lean manufacturing. This allows you to identify sources of waste at different stages of the production process and eliminate stages or individual operations that do not contribute to the profitability of the company. The latter, in turn, increases the profitability of transactions with distributors and makes it possible to bring the greatest benefit to consumers.

Improving the performance of an organization and advising on business operations and its support functions is one of the core competencies of SCM Consult.

Efficient distribution of goods is an important aspect for both manufacturers and wholesalers and retail. Moreover, organizations operating within the same distribution channel join forces to achieve more high level distribution of products through various methods of supply chain management. To find the most effective ways transportation of goods from the manufacturer to the enterprise wholesale trade and from the wholesaler to the retail stores, software-based analysis is performed.

Efficient routing and delivery planning are common aspects of efficient distribution. Some organizations resort to unusual ways of eliminating waste and sources of inefficiency. Thus, non-competing enterprises share the cargo space of vehicles for the passing transport of goods, thus avoiding losses from the movement of an incompletely loaded vehicle.

Inventory management is a key aspect for all participants in the distribution channel. Many distribution channels have already switched to new ways of working according to the Just-in-Time concept. Resellers and resellers want their firms to have just enough inventory to meet immediate demand.

Excess inventory leads to additional costs for management, relocation, and sometimes disposal. Therefore, manufacturers must be careful to produce the volume that matches the demand. Resellers buy the volume they expect to sell quickly. To avoid running out of inventory at the same time, potentially losing customers, companies have to maintain this delicate balance.

Services for segmentation and classification of competitive factors of production (OWC - Order winning criteria & OQ - Order qualifiers).

Services for the development of standard operating procedures of the company (SOP - Standard Operations Procedures) within the framework of corporate and marketing strategies organizations.

Process mapping and selection of optimal schemes.

Services for capacity management and bottlenecks in the company's production processes.

SPC (Statistical Process Control) - statistical power control, FMEA - Failure Mode & Effects Analysis analysis of failure modes and effects, Six Sigma.

Services for the development and implementation of operational strategy.

Preparation of gap analyzes between the market and the organization's operations, identifying key issues and identifying ways to improve performance.

Services for the implementation of lean manufacturing technologies Lean, 6 Sigma, JIT (Just-In-Time), Kaizen

, and other process improvement methods.Determination of target parameters (KPI) within the framework of key operational objectives, such as cost, reliability, flexibility, quality and efficiency.

Demand and Inventory Planning Services.

Working with operating staff.

Implementation of performance monitoring.

TQM (Total Quality Management) - comprehensive quality management

With the seeming abundance of business concepts in the world, there are not so many management systems that offer real methods for improving efficiency. One of the methods recognized in world practice to increase the operational efficiency of enterprises without significant financial investments is the concept of Lean production, in the Russian version of the translation "Lean production"

Theory, many practical exercises, case studies, feedback and personal recommendations

Company performance management

Key concepts, principles of lean production. Implementation examples

Practice:

Evaluation of possible initiatives, projects that are expedient to implement in the participating companies using lean manufacturing tools

Building a tree of goals for participating companies that must be achieved as a result of the implementation of lean manufacturing projects

Value stream mapping

Practice:

Development of a program for the implementation of the project "Value Stream Mapping"

Development of a VSM map for the production processes of students. Finding solutions to reduce losses

The system of organization and rationalization of 5S workplaces in production and in the office

Practice:

Development of a project plan for the implementation of the 5S system in production and in the office

Visualization. Examples of visualization solutions

Practice:

Development of a project plan to visualize the planning of repair work, work to improve processes

Poka-Yoka Error Prevention Method

Practice:

Considering practical examples of applying the 5 why method and Ishikawa diagrams

Organization of the work of analysis groups to reduce scrap, reduce equipment downtime, reduce emergency repairs

Consideration of practical examples of the application of the FMEA method

Using the concept of Enterprise Asset Management (EAM) in order to effectively use assets (equipment, Vehicle) enterprises

Practice:

Analysis of Western and Russian EAM systems

System continuous improvements"Kaizen"

Practice:

Application in practice of methods of statistical analysis

Optimization and standardization of business and production processes, procedures

Practice:

Development of a typical process based on the SIPOC diagram

Standard Operating Procedures (SOP)

Goals, objectives, components of the SOP

Analysis of examples of SOPs applied by foreign and domestic companies

Development of a standard operating procedure format for a company of trainees

Development of a project plan for the implementation of SOPs in the enterprise

General Equipment Maintenance System (Total Operational System) - TPM

Practice:

Development of a project plan for the implementation of a universal service system

Fight against the main types of losses. Cost Reduction Programs

Experience of foreign and Russian companies in the implementation of projects "Lean production"

Increasing the involvement of personnel in the process of implementing lean manufacturing solutions

Workshop:

Development of a motivation system for personnel involved in projects for the implementation of lean manufacturing solutions

Development of a KPI system for departments of the listeners' companies

Approaches to the implementation of lean manufacturing

Practice:

Development of a list of measures aimed at reducing costs and hidden losses for the student companies

Development of a plan for the implementation of lean manufacturing for the company of students

Anna Vasina, Head of Department economic analysis, Research and consulting firm "ALT", St. Petersburg

Cost reduction - the permanent "hit" of financial management

Today, in conditions of high competition, the companies that are able to conduct their business most effectively survive and develop. One of the main criteria for the effectiveness of doing business is the profit received. Reducing costs is the most important reserve for optimizing profits, reducing product prices, and, consequently, increasing the competitiveness and financial stability of the company.

In recent years, cost reduction programs have been implemented by companies of all industries and sizes (recall the cost reduction programs of Gazprom, RAO "UES", AVTOVAZ, and UAZ, which are widely covered in the press). The focus of cost reduction projects is very diverse - in particular, it is

Projects of various industries - the myth of uniqueness

To make a decision on the implementation of a particular project (idea), it is necessary to calculate and evaluate the economic effect - the profit that the company will receive in connection with the implementation of this project (idea). It is not uncommon to encounter the fact that the approach to evaluating the effect of cost reduction projects is associated with a specific product or industry.

For example, when providing services for the development of business plans, we hear the following statement of the question from the side of enterprises: "We need to develop a business plan for creating our own energy facilities. What CHP projects does your company have experience in evaluating - gas or solid fuel? We need a calculation on gas-fired CHP; if you "worked with fuel oil", then this experience is not suitable for us." Another case (of many similar ones): based on the results of a consulting project, we place on the Internet a description of an example of a motorcycle company that is mastering the production of an engine at its own production facilities. At the same time, in the section of reviews and recommendations for the posted materials, we read the following: “Low applicability of the material. Are there many motorcycle enterprises in Russia? We represent a completely different industry - the food industry - and now we are going to introduce packaging production at our enterprise. project, as the food industry is actively developing and such an example could be useful to more specialists." In other words, often the study of the project evaluation methodology turns into a search for a specific calculation template for a specific product or industry.

In the case of evaluating the effect of cost reduction projects (as well as other areas of profit optimization), the idea voiced in Paulo Coelho, so popular today, is absolutely true: "There is no need to understand the entire desert - one grain of sand is enough to see all the wonders of creation." Indeed, the definition of the effect of any project is based on the same approach, independent of the industry.

Cost reduction: a key approach to determining the impact

The economic effect of any project, including a cost reduction project, lies in the additional profit received. Additional profit, in turn, is determined by how much the company's revenue, production costs, and tax payments will change in connection with the implementation of this investment idea. Thus, the key approach to calculating the effect of any project (including cost reduction) is to determine how much more the company will receive and how much more it will pay in connection with the implementation of the project (see Figures 1 and 2).

Changes occurring in connection with the implementation of the project are determined on the basis of an analysis of the scheme of its (project) implementation, in particular, an analysis of changes:

Changes in the nomenclature, prices and sales volumes of products caused by the investment idea will make it possible to determine the desired changes in sales proceeds. Changes in the nomenclature, consumption rates and prices for consumed resources are the basis for calculating changes in the total value of variable costs for production. Transformations in production and organizational structure will allow you to determine changes in the fixed costs of the enterprise, in particular: the cost of wages, repair and maintenance of equipment and premises, utility bills. The purchase or sale of equipment, the construction or sale of fixed assets will entail a change in depreciation, property tax and the already mentioned costs for the repair and maintenance of the company's assets.

This approach is transparent, universal and correct for any situation. For example, in connection with the construction of its own thermal power plant, the following changes occur: the company ceases to bear the cost of purchasing energy, but "receives" new costs for the purchase of gas (solid fuel). The amount of expenses for the purchase of energy depends on the volume of energy consumption by the company and the cost per unit of resource set by the regional supplier. The amount of payments for gas (solid fuel) depends on the same volume of energy consumption by the company, as well as on the existing norms of gas consumption for the production of a unit of energy and gas (solid fuel) prices. There are no other changes in the technological chain (the chain of production of the final product sold by the enterprise); the production program is formed in the same way as before. Thus, the idea will lead to the following changes in revenue, costs and taxes (see the approach in Table 1.1 and an example of calculation on specific values in Table 3):

Similarly, describing the changes that will take place in a motorcycle enterprise in connection with the introduction of the production of engines on its own, we get the following picture: the company ceases to bear the cost of purchasing a certain number of engines on the side and begins to produce it on its own, spending certain money on the purchase of raw materials, components , energy. At the same time, there are no other changes along the technological chain, the production program is formed in the same way as before. The company will experience the following changes in revenue, costs, and taxes (see Table 2):

By carefully analyzing the key approach to assessing the impact of projects, as well as the examples proposed above, it is possible to obtain confirmation of the following: there are no project types as such

but there is a single type of investment idea, a single task - "the choice: to produce at home or to buy on the side" (often this task sounds like "assessment of the feasibility of organizing production at home with the refusal to purchase on the side"). The effect of projects of this type is determined in the same way, according to an identical algorithm. The differences will consist only in the names (products, production costs) and absolute values (prices, consumption rates), which is clearly demonstrated by the examples of tables 1.1 and 2.

It is also necessary to understand that the assessment of the effect of a CHP construction project on gas, fuel oil, coal is carried out in an absolutely identical way, and there is no need to search for three different calculation algorithms. The differences between the listed options will be only in absolute values - the price of energy resources in the region, the consumption rate and the cost per unit of gas, fuel oil, coal consumption. There may also be differences in the costs of repairing the fixed assets of the energy sector (depending on the equipment) and remuneration of the personnel of the energy sector (depending, for example, on the region). To correctly determine the effect in this case, it will be useful to know the key approach to calculating the effect. The search for analogues of the calculations "CHP on coal", "CHP on gas" will not be of greater value than studying the methodology, since in Russia there is a significant spread in prices for energy resources depending on the region and essentially identical projects in different regions will have different economic the effect.

The task of choosing "to produce in-house or to buy on the side" also includes outsourcing projects that are so popular today - the refusal of own production of some products and services with the transition to their purchase from third-party companies. Determining the effect of outsourcing projects, as well as any other optimization ideas, is based on the calculation of changes in income and costs associated with its (project) implementation.

In particular, if a motorcycle company evaluates the feasibility of abandoning the production of an engine on its own and switching to purchasing them from third-party suppliers (suppliers of similar engines exist and are ready to cooperate with the company), then they will see the following picture of changes in income, costs, taxes:

In determining the effect of the project, the components of the calculations of Table 2 will appear, but changes in property tax, variable and fixed costs will change their signs to the opposite.

Thus, qualifications in assessing the effect of cost reduction projects lie more in general than in details. Of course, knowledge of the specifics of the industry and enterprise is necessary, however, this information is required at the second stage of work - at the stage of "filling" the basic scheme for calculating the effect.

Important comments on cost benefit calculations

The description of the key approach to calculating the effect of cost reduction projects (as well as any projects aimed at optimizing profits) must be accompanied by important comments. In particular, the changes in revenue, costs and taxes that will be considered in determining the effect of the project should be:

To determine the effect that a company will receive in connection with a specific optimization idea (project, program), it is necessary to single out only those changes in revenue, costs, taxes that are caused by this particular idea (project, program). Otherwise, we will get the substitution of the project effect by the cumulative result of the company's activities, which will not allow us to correctly assess the need to implement a specific optimization idea.

For example, the construction of own energy sources is carried out in parallel with the growth in production and sales finished products(the marketing service has achieved attraction of additional orders). When determining the additional profit that the company will receive precisely in connection with the commissioning of its own thermal power plant, the increase in revenue from the sale of products should not be considered. The increase in sales volumes is not caused by the CHPP construction project, but is the result of the work of the marketing department. Sales growth will occur regardless of whether we buy energy on the side or produce it ourselves. The effect of building an own CHP plant will be to change costs and taxes - the changes discussed in Tables 1.1 and 3.

The growth in production volumes will affect the profit of the CHP project, but not through sales revenue, but through an increase in energy consumption and a corresponding increase in savings from reducing the costs of their (energy) production. In other words, in the calculation algorithm of Table 1.1, the volume of energy consumption will increase as the volume of production increases. The growth in sales revenue will be taken into account when modeling the company's current account and will allow, for example, to understand how much funds (money) from current activities the company can allocate to finance the CHP project. However, it is worth clearly distinguishing between the calculation of the effect (profit) of the project and the formation of a settlement account: the effect is determined by the changes caused specifically by this project, the final settlement account of the company, of course, is formed taking into account all changes - related and not related to the project in question.

Thus, in the examples of Tables 1.1 and 2, there is no change in revenue, not because the company does not plan to increase sales volumes, but because any changes in revenue are not a consequence of the project for organizing energy and engine production (an increase or decrease in sales volumes will affect the project through growth or a reduction in energy and motor consumption, hence through an increase or reduction in variable cost changes).

Another common example in this area is the determination of project investment cost performance indicators based on the overall flows of the enterprise with the project. The description of the general flows of the company before the implementation of the project and, further, the flows after the implementation of the project are absolutely correct in terms of modeling the current account, assessing the need for financing, and building a financing schedule. However, the total flows of the project and the enterprise will not allow you to correctly determine the effect (profit) of the project and the effectiveness of investments (payback, return on investment) - in most cases, you will receive significantly overestimated indicators in relation to the real possibilities of the project. The reason for the overestimated indicators will be the above-mentioned substitution of the effect of the project by the total result of the company's activities, where there are changes that arise due to other actions, projects, factors.

For example, companies using the total flows of the enterprise with the project when assessing the effectiveness of investments in the construction of their own CHP received a payback period of 1.5-2.5 years [Investment / Annual profit of the company, which changes due to the commissioning of the CHP]. The calculation based on the analysis of changes in costs caused by the commissioning of our own CHP showed a real payback period of 4.5 - 6.5 years [Investment / Annual additional profit, determined according to the principle of Tables 1.1 and 3].

To determine what changes in income, costs, taxes should be taken into account or not taken into account when calculating the effect of a particular project, you can use a simple and universal rule: if any changes in income, costs, taxes occur (or could occur) regardless of the project under consideration, these changes are not a consequence of the project and should not be considered when calculating its effect. If any changes in income, costs, taxes occur precisely as a result of the implementation of the project (and could not have occurred without its implementation), these changes should be taken into account when calculating the effect.

Another common calculation error is the assignment of a part of the existing costs of the enterprise to the project. Most often, this approach is found in projects involving the use of the company's existing production assets. In particular, in the project for the introduction of engine production, part of the technological operations will be performed on the already existing equipment of the enterprise. In this regard, one can hear the following reasoning: "part of the cost of maintaining this equipment, part of its depreciation should now fall not only on existing, but also on new products - the engine." These arguments are correct when calculating the cost of various products of the enterprise, but are not correct when determining the effect of the project.

The profit of the enterprise changes as a result absolute increases or decreases in income and costs, but not as a result of their redistribution. From the point of view of the total profit of the company, it does not matter how much of the depreciation and maintenance costs of the machine is allocated to a particular product. What matters is how much these costs rise or fall overall. For the existing equipment that will be used in the production of the engine, the amount of depreciation deductions will definitely not change (whatever the equipment load, depreciation is charged regularly, based on existing standards). There may be some increase in equipment repair costs - increased utilization may require more frequent repairs, hence higher costs per time period. Thus, in the calculation of the effect of the project, the "engine" should appear an increase in the cost of maintaining and repairing existing equipment, which will reflect the accounting of the company's existing funds involved in the implementation of the project.

Changes occurring at any stage of the production process will eventually lead to a change in the profits of the company as a whole. Thus, when considering any project, it is necessary to analyze the enterprise "as a whole".

Individual comments requires a description of the costs of production: it is desirable to separately consider changes in variables and separately - changes in fixed costs. Wherein variable costs are traditionally determined on the basis of unit costs per unit of output (determined on the basis of cost rates and prices per unit of resources). Description fixed costs, it is desirable to keep the individual elements of costs in absolute values for a period of time.(For example, the wage fund for auxiliary workers, whose number increases in connection with the implementation of the project, increases by N thousand rubles per month. For fixed assets sold in connection with the abandonment of auxiliary production, repair and maintenance costs will be reduced by Y thousand . rub per month).

The use of the cost of a unit of production may not always give an adequate assessment of changes in profit in connection with the implementation of an investment project. The cost price combines and redistributes costs; redistribution does not always make it possible to determine the absolute value of the changes. In addition, this approach is convenient and illustrative when preparing information for calculations. In particular, the description of fixed costs in most companies is carried out in the statements (budgets) of general workshop and general factory costs precisely in the context of cost elements in absolute values for the reporting period.

Key approach in action: some practical examples

The presentation of any technique is incomplete without demonstrating its application in practice. For the practical part, two rather relevant topics were chosen - the allocation of auxiliary (non-core) industries and the creation of their own energy sector (an example of heat production). Once again, we note that these examples are only variants of standard tasks (in particular, to make the choice "to produce in-house or purchase from outside") and do not have industry and product affiliation.

Creation of own energy economy

The first step in evaluating any idea is to identify the parameters that will change in connection with the implementation of the considered idea. In particular, when organizing the production of thermal energy at its own production facilities, the following changes in income, costs, taxes will occur:

The value of "future" costs consists of the costs of purchasing gas (gas consumption rate per 1000 Gcal * Price per 1000 cubic meters of gas * Volume of "replaced" energy), as well as the costs of maintaining the created energy facilities.

Existing costs for the purchase of thermal energy are determined based on actual data on the purchase price of thermal energy (per unit) from an existing supplier and the volume of energy consumption.

Thus, as a result of the project implementation, the costs and taxes of the enterprise will change in the following volume:

It should be noted that the volume of consumed energy resources that is "not replaced" by the energy produced by the own CHP (140,000 + 100,000-190,000 = 50,000 Gcal.) is not considered when describing the effect of the project. The costs of purchasing this volume of energy resources will not change: energy continues to be purchased on the side from N-energo at the established tariff.

The resulting increase in profit will become the basis for calculating the payback period of investments [Investment / Profit growth (for the year) + Depreciation (for the year)] and other components of the assessment of the effectiveness of investment costs /

Transformations affecting ancillary industries ( non-core assets)

One of the currently relevant areas of profit optimization is the transformation affecting auxiliary production, non-core assets. In this case, the set of alternatives itself may merit special attention; the effect of each alternative is determined using a standard key approach.

We can single out the following alternatives for the development of auxiliary industries (VsPr), non-core assets:

The effect of allocating funds to a separate enterprise is determined using the algorithm of the "Assets sale" option (Table 6). The difference will be in the absence of one-time income from the sale of assets. H

It must be remembered that in this case there is another interested party - the holding, for which the effect of manipulations with auxiliary production will look different. The costs of maintaining and operating auxiliary production shops will "transfer" from one enterprise to a newly created structure. Thus, from the point of view of the holding, there may not be any fundamental changes in the costs of maintaining and operating auxiliary production. The fixed costs of the newly created enterprise will increase slightly compared to the workshop costs of auxiliary industries of the existing enterprise. This is due, in particular, to the appearance of administrative costs (a new enterprise will probably require the creation of an administrative and managerial apparatus). The additional profit of the holding, as well as the profit of the newly created enterprise, will be created by an additional volume of sales of products, which the newly created structure should be aimed at. That is, when determining the effect of the considered alternative from the point of view of the holding, the algorithm of the option "Additional loading of funds" (Table 4) will be useful.

Once again about the key approach to determining the effect

As it turned out above, the methodology for calculating additional profit has no industry restrictions, and the effect of cost reduction projects in metallurgy, mechanical engineering, and the food industry is determined according to the same principle. It is important to add that the methodology for calculating additional profit has no restrictions on the direction of projects - that is, it is absolutely fair both for projects to reduce costs and for projects to increase production volumes (in particular, this point became obvious when describing the effect of additional loading of auxiliary production).

In order to once again prove the absence of "industry binding" of any projects (not just cost reduction projects), let's consider the main types of ideas (programs) for profit optimization that companies have to deal with at various stages of work.

From the point of view of the specifics of the description of income and costs, three main types of projects can be distinguished:

After analyzing the essence of any project (for example, the introduction of PMIS, expanding the distribution network, investing in a brand, building its own refinery by an oil producing company), you can find that the project belongs to one of the three types listed (implementation of PMIS - cost reduction; expansion of the marketing network and investments into a trademark - expansion of production; construction of its own refinery - consumption of petroleum products at home with their sale to the side).

Having a key approach to evaluating the effect, it is possible to clearly present the algorithm for calculating the effect of each of the listed types of projects:

Reducing costs in conjunction with the implementation of the resource to the side(this type of project involves the refusal to purchase a resource on the side and the organization of its production at home; in addition to the consumption of the resource by the company, it becomes possible to sell part of the produced resource to third-party enterprises)

Key Decision Factors

When making a decision on the implementation of a particular project (programs, ideas, alternatives), a combination of factors - economic and organizational - is taken into account. The economic factor of decision-making lies, first of all, in the volumes of additionally received profit and indicators of "return" of investment costs. The above arguments about the methodology for determining the effect of various projects should be accompanied by an important practical commentary: calculations should be based on real market information. This applies, first of all, to the amount of additional revenue received from sales.

In particular, in projects for the separation of auxiliary production facilities for the purpose of additional loading, the additional revenue received often based on data on the production capacity of the equipment, which can overestimate (sometimes significantly) additional income. Evaluation of additional orders that the company is really able to attract, should be based on data about specific buyers, having the intention to purchase products of auxiliary industries of this enterprise. Thus, one of the components of the project evaluation work, of course, is the study of the consumer market (and specific consumers).

There are a number organizational factors which will be of fundamental importance when deciding on the implementation of the project. For example, all in the same project of separation of auxiliary productions into a separate enterprise, such an important factor is the presence of an effective management team. A team that is able to effectively organize the work of the newly created unit (including the ability to attract orders, form an action plan to increase competitiveness and strengthen the market position, clearly organize work "inside" the new unit).

It is obvious that consideration of the alternative of "giving up production in-house and switching to procurement from outside" will not be possible in the absence of an alternative supplier (which is observed for unique products or services). Legislative restrictions on the implementation of one or another alternative are also possible (for example, existing restrictions on the issue of "resale" of electrical energy).

As a result, we can say that choosing and making an effective decision in any field is an art, and it is difficult to argue with the statement that "there are no formulas at the top." However, the adoption of any decision is impossible without the possession of reliable information, including economic information. The reliability of the presented economic information is largely determined by understanding the essence of economic processes, knowledge of specific methods and approaches. Thus, knowledge of the "formulas" can also contribute to the movement to the "top", at least to the top of professionalism.

The purpose of a commercial enterprise is to make a profit. The company earns its income from the sale of goods and...

A duopoly is a market structure in which two sellers, protected from the emergence of additional sellers, are...

The term oligopoly comes from the Greek words oligos (several) and poleo (sell). Fundamental...

The simplest oligopolistic situation is when there are only two competing firms in the market. Home...

Competition dominated by only one or a few firms. Today, a good example is the market...

In a competitive environment, the most important property is the competitiveness of the company, and it is to ensure that ...

Other factors also influence supply: 1. Prices for resources. 3. Technology. 4. Taxes and subsidies. 5. Prices...

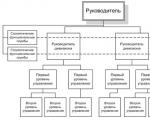

This type of organizational structure is the development of a linear one and is designed to eliminate one of its shortcomings, ...

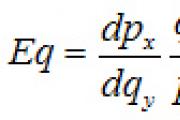

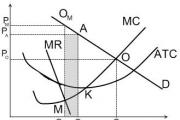

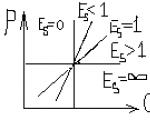

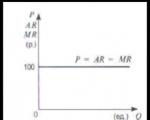

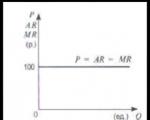

Marginal revenue Marginal revenue (MR) is the revenue generated from the sale of...

Marginal revenue Marginal revenue (MR) is the revenue generated from the sale of...

The term "monopoly" is one of the most capacious in economic theory. The correctness of its use is largely ...

What is a guiding question? The guiding question is a question about: - value; - importance; - usefulness of the decision. Why ...

The second half of the 20th century was marked by a scientific and technological revolution in the world, which also affected shipbuilding. On the...

The six handshake theory is the theory that any two people on Earth are separated by an average of only five...

13 In this article we will talk about how to find out the track number of the parcel on the Aliexpress website. Nothing complicated...

The holiday is dedicated to all those who are waiting with great excitement for the New Year, Santa Claus and the cherished ...